What is acquisition financing?

Acquisition financing is the capital a buyer uses to purchase another business, a business division, or a set of business assets.

In practice, it usually refers to a business acquisition loan or a mix of funding sources used to complete the transaction.

Key takeaways:

- Acquisition financing helps you buy a business without paying the full purchase price in cash

- Common options include SBA 7(a) loans, conventional bank loans, seller financing, mezzanine financing, and equity

- Buyers typically contribute 10% to 30% of the purchase price as a down payment or equity injection

- Loan terms often range from seven to 10 years, and longer terms may apply when real estate is part of the deal

- Closing timelines usually fall between 30 and 90 days, depending on the lender and deal complexity

At a high level, acquisition financing works by using the target company's expected cash flow, assets, and overall deal structure to support repayment.

A lender evaluates the buyer, the business being acquired, and the strength of the transaction before issuing an acquisition loan.

Many deals use a layered capital structure rather than a single source of funding. For example, you might combine an SBA loan with a cash down payment and a seller note.

This can reduce upfront cash requirements while improving the overall financing package.

This matters because the right financing structure can make an acquisition more affordable, preserve working capital, and give your combined company enough flexibility to operate comfortably after closing.

Done right, acquisition financing fuels growth. Done poorly, it can sink the whole ship.

How to secure acquisition financing: A step-by-step process

Securing acquisition financing is easier to manage when you break it into clear stages.

Most buyers move through the same core process, from preparing financials to closing the loan.

Step 1: Prepare your financials and deal story

Start by assembling the documents lenders will expect to review. This usually includes:

- Personal and business tax returns

- Historical financial statements

- Bank statements

- A personal financial statement

- Details on the target company's revenue, profit, and cash flow

- A summary of how the acquisition will be financed and managed after closing

This stage often takes two to four weeks, depending on how quickly information can be gathered.

Step 2: Build the right financing mix

Most acquisitions are funded through more than one source. A common structure might include:

- An SBA 7(a) loan or bank loan for the majority of the purchase price

- A buyer cash contribution for the down payment

- A seller note to bridge the remaining gap

At this stage, you should also confirm whether you have enough post-close working capital.

A strong structure does more than get the deal approved—it also helps the business operate smoothly after the transaction closes.

Step 3: Submit applications and lender packages

Once the financing structure is clear, submit a complete package to one or more lenders. A typical acquisition financing package includes:

- Signed LOI or purchase agreement

- Historical and projected financials

- Debt schedule

- Business plan or acquisition thesis

- Information on management experience

- Details on collateral, if applicable

This stage often takes one to two weeks, though strong preparation can shorten it.

Step 4: Move through underwriting

Underwriting is the point where lenders validate the strength of the deal. They'll often assess:

- Credit score and personal liquidity

- Industry or management experience

- Debt service coverage ratio (DSCR)

- Quality and stability of cash flow

- Purchase price support, including valuation

- Working capital needs after closing

You should expect requests for follow-up documentation. Underwriting typically takes four to eight weeks, and delays often happen when financials are incomplete or deal assumptions are unclear.

Step 5: Close the transaction

After approval, the lender, attorneys, and seller finalize loan documents and closing requirements. You should budget for:

- Lender fees

- Legal fees

- Valuation or quality of earnings reports

- Filing fees and other transaction costs

Closing usually takes one to two weeks once final approval is issued. In total, many acquisition loans close within 30 to 90 days, depending on the lender, the program, and the complexity of the deal.

Types of acquisition financing

As CFO, you have a number of routes to consider when financing an acquisition. So, let's walk through some of the common options:

1. Stock swap transaction

Using company shares instead of cash to buy another business lets you expand without draining your cash reserves. It shows you've got faith in the new mega-company you're creating too.

Example: Company A offers 0.5 shares of its stock for every share of Company B. If Company B has 1 million shares outstanding, Company A issues 500,000 new shares to complete the deal. No cash changes hands, and Company B's shareholders become part-owners of the combined entity.

2. Equity acquisition

This involves the acquirer paying for the target company by issuing new shares of its own stock to the target's shareholders.

It's similar to a stock swap but focuses on expanding the ownership base to include the shareholders of the acquired company. Taking this route dilutes the existing shareholders' stakes but avoids increasing the company's debt load.

Example: A tech startup acquires a smaller competitor by issuing 200,000 new shares to the competitor's founders, giving them a 15% stake in the combined company.

3. Acquisition through debt

Borrowing money is probably the most affordable way to buy another business. Banks will lend company acquisition money through loans, bonds, etc.

Debt financing makes it possible to make large acquisitions without diluting shareholders' equity, but it increases the company's leverage and financial risk.

Example: A manufacturing company secures a $10 million term loan from a regional bank to acquire a supplier, using the supplier's equipment as collateral.

4. Leveraged Buyout (LBO)

Here, most of the money needed to acquire the target company comes from loans backed by the assets being acquired. LBOs are a high-risk, high-reward strategy, often used by private equity firms.

Example: A private equity firm acquires a restaurant chain for $50 million, putting up $10 million in equity and borrowing $40 million against the chain's real estate and cash flows.

5. Cash acquisition

A straightforward method where the acquiring company pays cash for the target company's shares. This is often preferred by the sellers because it provides immediate liquidity.

For the buyer, it means using either available cash reserves or raising new capital specifically for the acquisition, potentially through issuing debt or equity.

Example: A retailer uses $5 million from its cash reserves to buy a regional competitor outright.

6. Seller’s financing / Vendor Take Back (VTB) Loan

In seller’s financing or VTB, the seller of the company extends a loan to the buyer to cover part of the purchase price.

This can be beneficial in the case where the buyer is unable to secure sufficient financing from other sources.

Example: You buy a local business for $1 million, paying $700,000 at closing and signing a note to pay the seller $300,000 over three years.

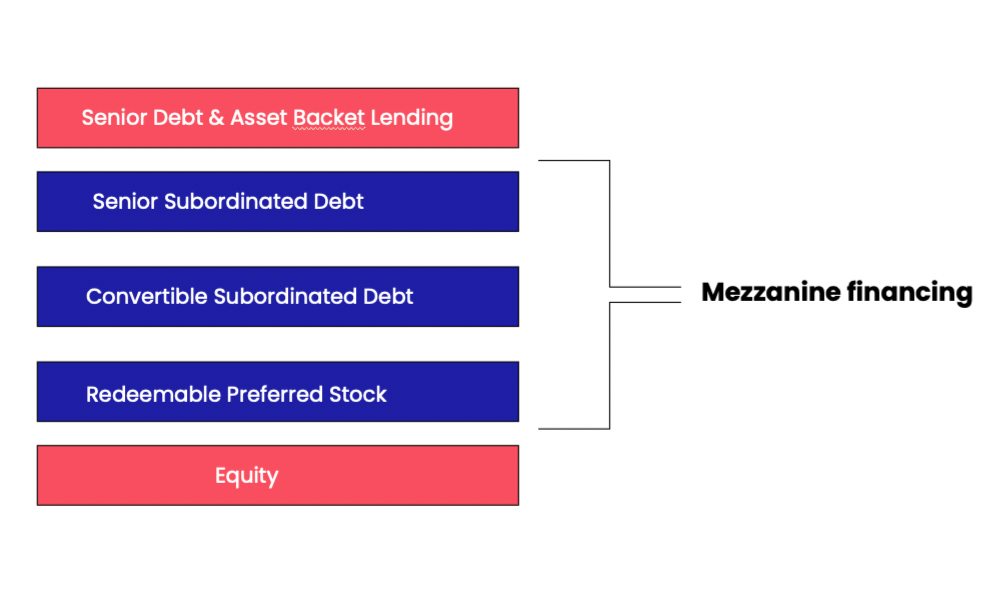

7. Mezzanine financing

Mezzanine financing is a hybrid form of capital that combines elements of debt and equity financing.

It provides lenders the right to convert to an ownership or equity interest in the company if the loan is not paid back in time and in full.

It’s often used to finance the expansion of existing companies and is subordinate to debt provided by senior lenders like banks.

Example: A company raises $3 million in mezzanine debt to bridge the gap between its bank loan and the equity it can contribute, giving the mezzanine lender warrants to purchase shares if the loan isn't repaid.

As Christopher Toumajian notes: "Even two deals that look almost identical compared to each other can have wildly different deal structures."

The takeaway is that blended structures are common. Many acquisitions combine cash, equity, seller financing, and debt in creative ways to balance risk, preserve cash flow, and align incentives between buyer and seller.

Mezzanine financing and subordinated debt in the M&A capital stack

When senior lenders cap how much they'll provide and equity alone can't bridge the gap, mezzanine financing and subordinated debt step in to complete the capital stack.

Understanding where these instruments sit (and why buyers use them) can make the difference between a deal that closes and one that falls apart.

The key feature: mezzanine debt is subordinated, meaning it sits below senior debt in the repayment hierarchy. If the company runs into trouble, senior lenders get paid first. Mezzanine lenders wait in line.

Subordinated debt, more broadly, refers to any debt that ranks below senior obligations. Mezzanine financing is one type, but subordinated notes and junior debt also fall into this category.

What makes mezzanine distinct is that it often includes equity kickers; warrants or conversion rights that let the lender convert their debt into ownership shares under certain conditions.

This sweetener compensates for the added risk of being lower in the capital stack.

Why do buyers use this layer? Three main reasons:

- It bridges funding gaps when senior lenders won't provide enough leverage.

- It reduces equity dilution; you're borrowing more instead of giving up ownership.

- It increases deal size, letting you pursue larger acquisitions than your equity and senior debt alone would support.

Here's how a typical M&A capital stack might look in practice. Imagine a $100 million acquisition. The buyer contributes $30 million in equity. A senior lender provides $50 million in term debt secured by the target's assets. That leaves a $20 million gap.

A mezzanine lender fills it with subordinated debt at 15% interest, plus warrants representing 3% of the company's equity.

The intercreditor agreement between the senior and mezzanine lenders spells out who gets paid when, and under what circumstances the mezzanine lender can take action if payments are missed.

The mechanics matter. Mezzanine debt typically has longer terms (five to seven years), often with interest-only payments in the early years and a balloon payment at maturity.

Repayment priority is clear: senior debt first, then mezzanine, then equity holders.

If you're structuring a deal with mezzanine financing, expect detailed negotiations around subordination terms, prepayment penalties, and the conditions under which warrants convert.

Debt vs equity financing: pros and cons when acquiring a business

Debt financing means borrowing money (through bank loans, bonds, or credit facilities) to fund an acquisition, while equity financing involves issuing new shares to raise capital or using stock as purchase consideration.

The core tradeoff comes down to control versus financial risk: debt preserves ownership but adds repayment pressure, while equity dilutes existing shareholders but keeps your balance sheet lighter.

So how do you decide which path fits your deal? Start with cash flow. If the target company generates strong, predictable cash flows, debt financing often makes sense because those revenues can service the loan payments.

Lenders will look at coverage ratios and want confidence that the combined entity can handle the new obligations.

On the other hand, if cash flows are uncertain or you're already carrying significant leverage, equity financing reduces the strain on your balance sheet and avoids covenant risk.

As Christopher Toumajian, Vice President of Corporate Development at EP Wealth Advisors, explains: "How much cash, how much equity are we offering in our deals? What's the impact of that on our cash flow forecasting?"

This consideration mix (the blend of cash and equity in your offer) shapes everything from deal structure to long-term capital planning.

A practical decision framework: lean toward debt when the target has stable EBITDA, your existing leverage is manageable, and you want to preserve shareholder value.

Lean toward equity when the deal size stretches your borrowing capacity, when market conditions make debt expensive, or when you want to align the seller's interests with long-term performance through stock consideration.

Many deals, of course, blend both, and that flexibility often produces the most resilient capital structures.

FAQs: Acquisition financing

Can seller financing count toward my down payment?

Usually, no. Most lenders still require you to contribute meaningful cash equity. Seller financing can strengthen your deal structure, but it typically won't fully replace your required down payment.

What interest rates should I expect?

Rates depend on the lender, your profile, and the deal structure. In general:

- SBA 7(a) loans often price at a spread above prime

- Conventional bank loans may offer competitive pricing for strong borrowers

- Alternative lenders tend to charge higher rates in exchange for speed or flexibility

Your final rate will depend on credit, cash flow, collateral, industry risk, and down payment size.

How much can I borrow for an acquisition?

Borrowing capacity depends on the financing program and the business's ability to support debt.

For example, SBA 7(a) loans can fund up to $5 million, while bank and non-bank options vary widely by lender and transaction profile.

How long does acquisition financing take?

Most acquisition loans close in 30 to 90 days. SBA and bank loans often take longer than alternative lending solutions because underwriting is more detailed and documentation requirements are heavier.

What will lenders look for in my application?

Lenders typically review:

- Your credit profile

- Your relevant business or industry experience

- The target company's historical cash flow

- Debt service coverage ratio (DSCR)

- Available collateral

- The reasonableness of the purchase price

- Your post-close liquidity and working capital position

Do I need collateral or a personal guarantee?

Often, yes. Many acquisition lenders require a personal guarantee, and some also require available collateral.

SBA and conventional lenders commonly take a lien on business assets, and some may look for additional collateral support depending on the transaction.

Become a Finance Alliance Pro member

Our Pro membership offers a unified source of trustworthy value for finance professionals to gain new knowledge. It's the all-in-one platform for finance professionals committed to lifelong learning, networking, and career advancement.

- Pre-built financial models

- Templates & frameworks

- 100+ hours of OnDemand insights

- FinIQ competency framework

- Mentor program

- Members-only networking & webinars

- Ungated access to reports

- Workshops & webinars

- Discounts on events

Secure your spot at the forefront of the finance industry with access to expert-driven tools and insights that promise to amplify your career trajectory.

Finance alliance insider

Thank you for subscribing

Level up your finance alliance career & network with finance alliance experts.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn