As a CFO, you're probably feeling the heat with all the talk about a looming recession, inflation, supply chain issues, and global instability.

It's times like these when your role becomes super important.

Your mission?

To cultivate resilience in economics. That means shaping a business model that's flexible and tough enough to handle whatever the economy throws your way.

You might be thinking, "Easier said than done," and you're not wrong. After all, the finance industry is known for its volatile nature, extreme ups and downs, and ever-changing variables.

However, with the right financial resilience strategies, mindset shifts, and execution tactics, developing true economic resilience is possible. Keep reading to find out how.

Topics covered:

- What makes a resilient economy?

- 11 tips to build financial resilience in business

- Financial economic resilience: Advice from the pros

- Economic resilience & agile leadership

- Economic predictions for 2024

What makes a resilient economy?

A financially resilient economy can withstand and recover from unexpected shocks or disruptions. There are a few key characteristics that foster economic resilience:

Diversification

Think about it – a one-trick pony is way more likely to stumble when the going gets tough. An economy that spreads its bets across different sectors and industries is way less likely to take a nosedive when one area hits a snag.

Strong financial systems

We're talking rock-solid banking and financial sectors that can take a hit without crumbling. Also, easy access to credit for businesses and individuals keeps the wheels turning, even when things get bumpy.

Adaptive capacity

It’s all about being able to pivot. Businesses, governments, and even you and me – we've all got to be ready to switch gears, embrace new tech, and shake up our game plans when needed.

Effective governance and institutions

Good governance is key. We need transparent, accountable institutions and effective policy-making to manage crises and drive reforms.

Social safety nets

When things go south, systems that help people out – like unemployment benefits and healthcare – can keep spending steady and stabilize the economy.

Robust infrastructure

Having solid physical and digital infrastructure in place means businesses can keep running smoothly, even when unexpected things like natural disasters or cyberattacks happen.

Human capital development

Investing in education and training is a no-brainer. It gears up the workforce to adapt to new industries and tech advancements, driving innovation.

Global integration with local autonomy

Being connected to the global economy has its perks, but it's also smart to have some self-reliance in critical areas like food, energy, and manufacturing to avoid getting tripped up by global supply chain issues.

Sustainable practices

Going green isn't just trendy – it's smart. By focusing on ESG efforts such as environmental care and renewable energy, you can help reduce reliance on finite resources and lessen climate-related risks.

Healthy public finances

Finally, having your financial house in order – think manageable debt and the ability to gather resources in a crisis – is crucial for stability and economic resilience.

11 tips to build financial resilience in business

Building financial resilience in business isn't just about bracing for a hit. It's about making sure your business stays on its feet and keeps moving forward, no matter what the economy throws at you. Here’s how you can do just that:

1. Strengthen your cash flow

Cash is king, right?

Make sure you're getting paid on time and keeping a good relationship with your suppliers. And it's smart to have a cash reserve tucked away for rainy days.

2. Diversify revenue streams

Don’t rely on just one thing. Explore new products, markets, or business models. It's all about not putting all your eggs in one basket.

3. Maintain a strong balance sheet

Keep an eye on your debts and assets. Smart borrowing and investing can boost your business’s growth and resilience.

4. Plan for the unexpected

Expect the best but prepare for the worst. Have plans ready for potential risks and keep updating them.

5. Invest in your people

Your team is your biggest asset. Training and developing their skills mean they’re ready to handle whatever comes their way.

6. Embrace technology and innovation

Stay ahead of the game with the latest tech. It can make your operations smoother and open new opportunities.

7. Build strong relationships

Solid relationships with suppliers, customers, and lenders can be a lifeline when times are tough.

8. Keep an eye on the market

Stay informed and be ready to adapt to industry trends and market changes.

9. Prioritize sustainability

Being eco-friendly can save you money, boost your brand, and open up new markets.

10. Regularly review financial health

Keeping a close eye on your financials helps you make smart decisions and tweak your strategies as needed.

11. Resilient financial planning

This is all about being ready for anything. You want to have a variety of income sources and a balance sheet that's in tip-top shape. It's like having a toolkit with all sorts of tools – you’re prepared for different kinds of jobs or challenges that may come up.

By taking these steps, you're not just setting up your business to survive the tough times; you're gearing it up to grow and flourish, no matter what the economic climate throws at you.

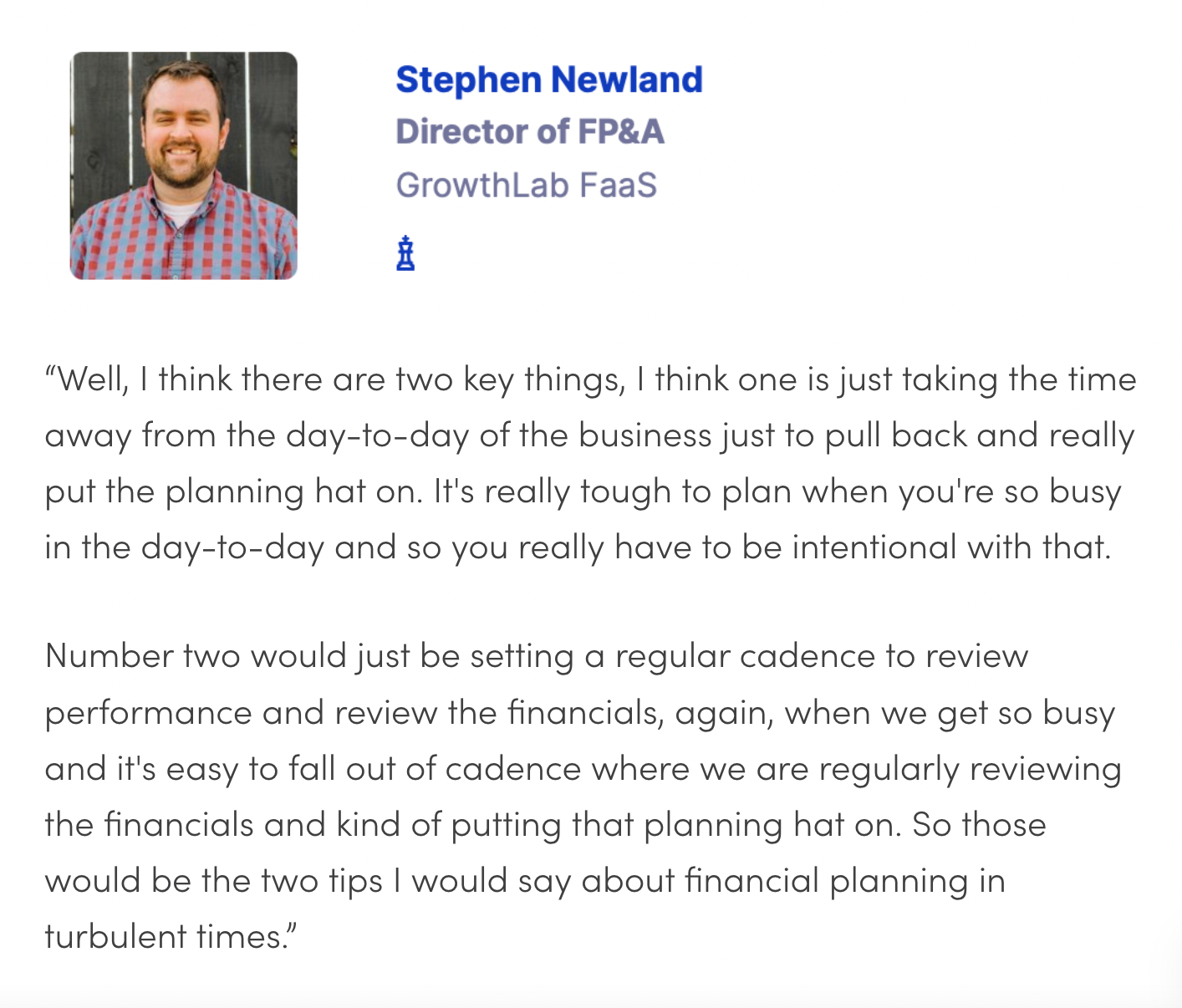

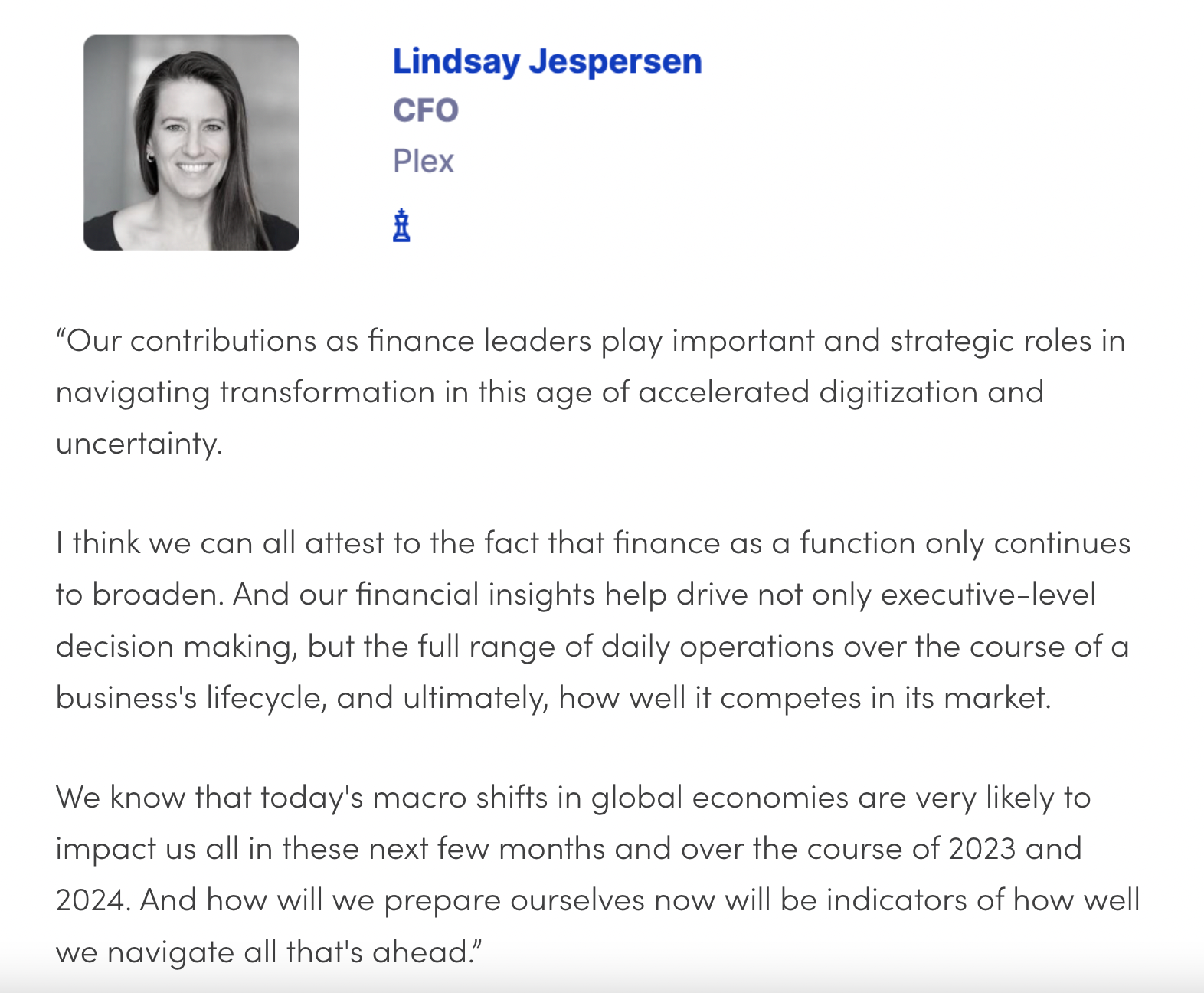

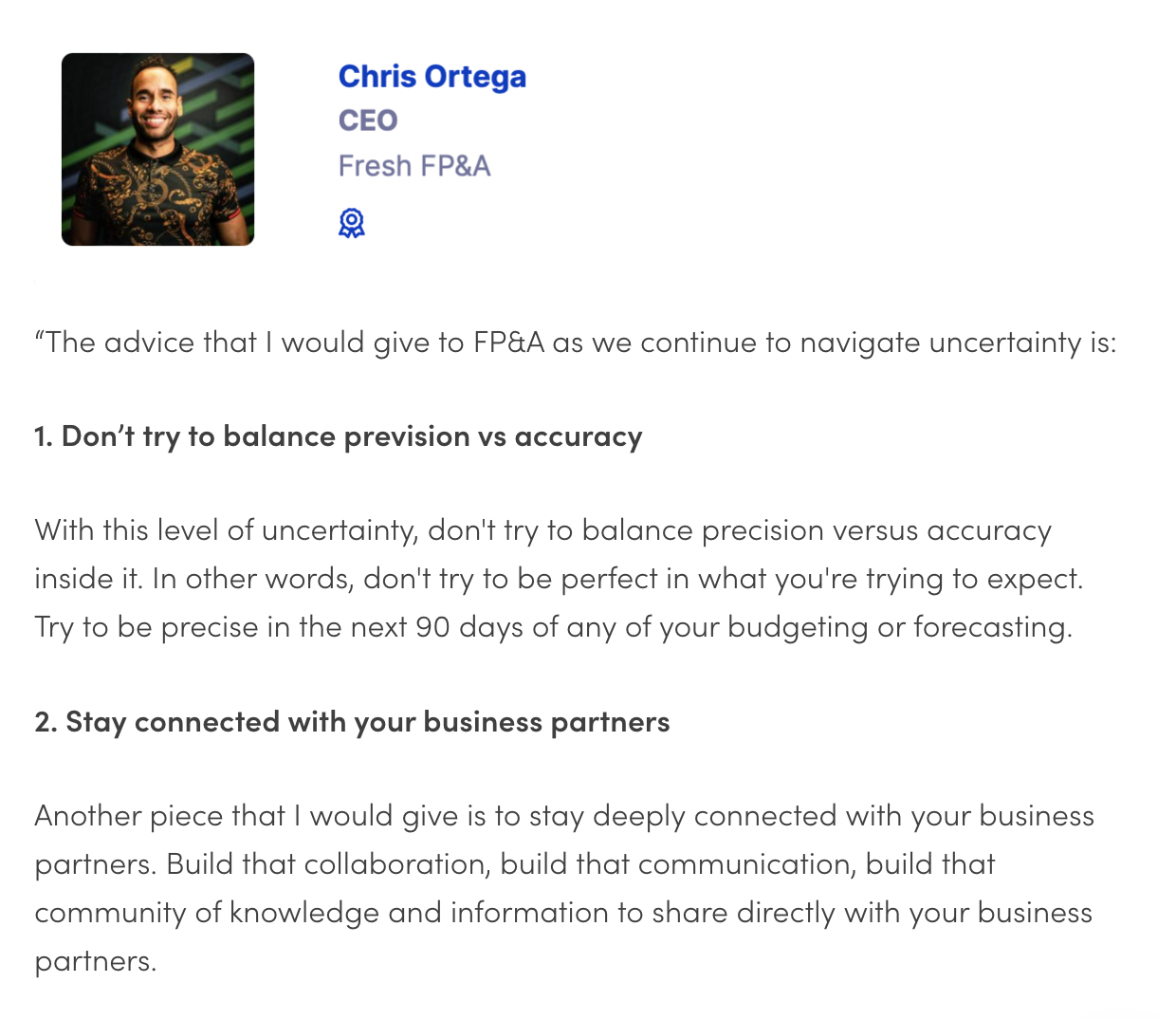

Financial economic resilience: Advice from the pros

Here are a few words of advice from members of our Finance Alliance community (including some of our great event speakers!):

Economic resilience & agile leadership

As a CFO, navigating through economic resilience isn’t just about crunching numbers and balancing budgets. It’s also about agile leadership – being that dynamic force that guides your team and company through the ups and downs of the economy.

Let’s face it, when the economic seas get rough, a rigid, “stick-to-the-plan-no-matter-what” approach just doesn’t cut it. You need to be agile, ready to make quick decisions, and open to shifting gears when necessary.

Being an agile leader means you’re always on your toes, looking out for both risks and opportunities. It’s not just about reacting quickly to changes; it’s also about anticipating them.

As a CFO, this might mean you're frequently reassessing financial forecasts, staying ahead of market trends, or even re-evaluating investment strategies to ensure they align with the current economic climate.

But agility isn’t just about what you do; it’s also about how you lead.

In uncertain times, your team looks to you for direction and reassurance. This is where your communication skills come into play. Being clear, transparent, and, most importantly, frequent with your communication can make a world of difference. It’s about keeping everyone in the loop, making sure they understand not just the 'what' and the 'how,' but also the 'why' behind decisions and changes.

An important part of being an agile leader is also understanding that resilience is a team sport. Investing in your team, and giving them the tools and skills they need to adapt and thrive, is crucial. It’s about creating an environment where learning, innovation, and flexibility are part of the daily routine. This way, when the unexpected hits, your team is not just ready to face it but can also find new and creative ways to overcome challenges.

Economic predictions for 2024

Looking ahead to 2024, economic forecasts suggest a mixed bag. FocusCFO states that a recession likely to begin toward the end of 2023 and persist throughout 2024. The high inflation experienced in the past 24 months is expected to wane during this period. However, this relief might be temporary, as inflation is forecasted to return in 2025 and remain a part of the economy for the rest of the decade

On the other hand, Fidelity International outlines a base case for a cyclical recession in 2024. Driven by fiscally supported consumers and companies, the economy has shown resilience, but signs indicate it will turn lower next year.

The savings buffer built up during the pandemic is nearly depleted, and with likely credit tightening and reduced fiscal support, a moderate recession seems probable. This scenario would be driven by tight monetary policy, normalizing labor markets, and eventually moving toward recovery by the end of 2024.

Beyond 2024, experts from ITR Economics predict a ‘second Great Depression’ in the 2030s:

“The road leading up to the Great Depression will be consequential in and of itself, with many opportunities and challenges. Business leaders need to be planning now for this period, as we all seek to maximize profits and enterprise value.” – ITR Economics

FAQs: Economic resilience

What is the key meaning of resilience?

Resilience is the ability to quickly recover from challenges and adapt to changes, maintaining functionality and stability in the face of difficulties.

What is socio-economic resilience?

Socio-economic resilience refers to the capacity of a community or society to withstand and recover from economic and social challenges, such as financial crises, natural disasters, or social disruptions.

What is economic resilience?

Economic resilience is the ability of a business to withstand and recover from economic challenges like recessions, market volatility, and other financial shocks.

How can CFOs improve cash flow management for resilience?

Improve cash flow by optimizing payment collections, managing payables efficiently, and maintaining an emergency cash reserve for unforeseen events.

What role does technology play in economic resilience?

Technology streamlines operations, improves efficiency, and opens up new business opportunities, all of which contribute to a stronger, more resilient business.

How does sustainability play a role in economic resilience?

Sustainable practices can lead to cost savings, create new business opportunities, and reduce reliance on finite resources, contributing to long-term economic stability and resilience.

Become an FA Insider

Thank you for subscribing

Get exclusive insights, frameworks, and strategies from finance leaders driving real business impact.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn