Believe it or not, a crisis management plan (CMP) is not the same as a business continuity plan (BCP). The two are similar in many ways, sure, but they have key differences that set them apart.

When disaster strikes and steers the business off course, it can lead to chaos, and in extreme cases, send the business into bankruptcy.

For finance teams, this means safeguarding liquidity and managing cash flow, and ensuring the business can weather the storm.

The good news is that you can help the business avoid such a catastrophic fate by creating and implementing both a business continuity plan and a robust crisis management plan.

And, even better, you can build them in such a way that they work effectively together to help prepare the business and guide it through any crisis.

So, if you want to know the main differences between a crisis management plan vs business continuity plan, keep reading!

What is a crisis?

Before we can compare the differences between a crisis management plan vs a business continuity plan, let's define what we mean by 'crisis.'

A crisis in the context of business is an event that disrupts the business's facilities such as data, personnel, IT systems, etc. This can then cause production to cease, which stops the business from running as it should.

The impact of a major crisis on a business can have a knock-on effect and negatively impact areas including production schedules, the business's reputation, customer advocacy, revenue, and so on.

Here are some examples of potential crises that could impact a business:

- Accidental disasters (power cuts, fires, gas leaks, etc.)

- Natural disasters (storms, hurricanes, floods, etc.)

- Technological disasters (corrupt software, faulty hardware, harmful cyber-attacks, etc.)

- Vandalism or theft

- Fuel shortages

- Loss of a staff member or a staff member being ill and unable to work

- Disease or widespread infection (COVID-19 is a prime example of this)

- Terrorist attack (local or abroad)

- Human error

- War

- Privacy policy issues

- Supply chain issues

- An industry strike

- Data protection issues

- Collapse of infrastructure

- Abandonment in leadership

The reality is, businesses face a wide range of potential threats, both predictable and unforeseen. Recognizing the variety of these potential disruptions underscores the critical need for proactive planning.

Without proper crisis management and business continuity strategies in place, companies are left vulnerable to significant, and potentially irreversible, damage.

What is a crisis management plan?

A crisis management plan (CMP) is a response plan to a crisis that would negatively impact the business's ability to operate or damage its reputation or profitability.

Businesses must be prepared to face different crises appropriately and crisis management plans act as guides to help navigate critical situations and avoid further catastrophes.

The plan should include a set of steps to help the business handle the crisis.

So, just how important is a crisis management plan?

One data point I keep coming back to: a FEMA statistic widely cited in disaster recovery coverage suggests 40% of businesses never reopen after a disaster.

That's why your crisis management plan needs to be specific about decision rights, communications, and cash actions before the first urgent call comes in.

To give your business the best possible chance of survival, you need a well-thought-out crisis management plan with specific steps to handle such an event.

What is a business continuity plan?

A business continuity plan (BCP) outlines how a business will continue to operate should an unplanned occurrence take place.

It's a comprehensive document that acts as a prevention and recovery system for potential threats or disruptions such as cyber-attacks or natural disasters.

The best BCPs are those that have been tested numerous times to make sure there are no gaps or weaknesses. And, if some weaknesses are identified during the testing process, those must be corrected.

This is to ensure personnel and assets are fully protected in the event of a crisis.

The main goal of a BCP is to provide the business with thorough strategies and information required to maintain operations throughout and following a disaster.

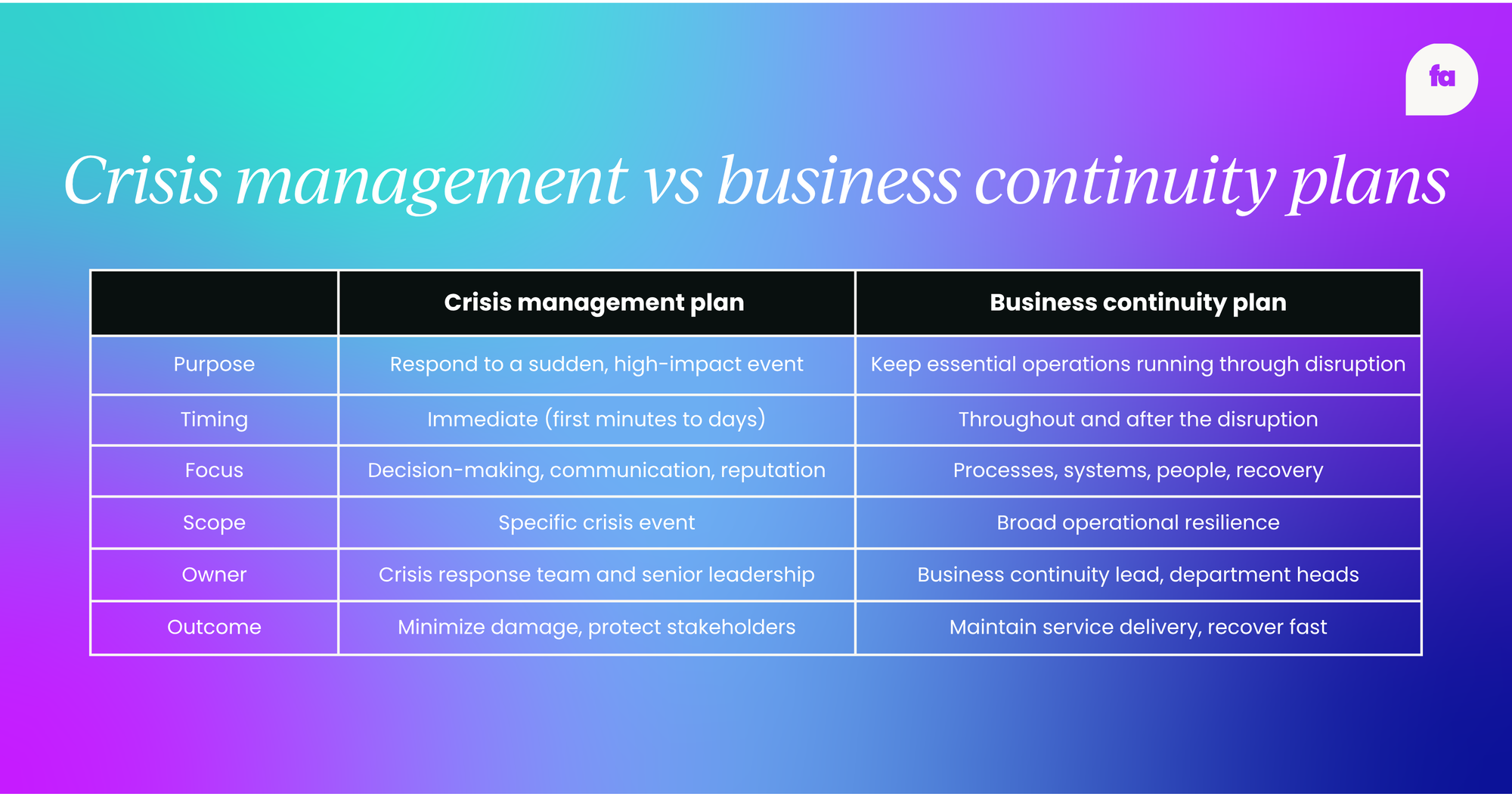

Crisis management plan vs business continuity plan: Key differences

So where do these two plans actually diverge? On the surface, they both deal with disruption. Dig a little deeper and you'll see they solve different problems at different points in time.

Here's a side-by-side breakdown:

Think of the CMP as what you reach for the moment something goes wrong. The BCP is what keeps the lights on while you're dealing with it.

A quick example. When COVID-19 hit, companies activated crisis management plans to communicate with staff, close offices, and address investor concerns.

Their business continuity plans handled the longer tail, including remote work infrastructure, supply chain rerouting, and cash flow protection. Two plans, one disruption.

For finance teams, the distinction matters. Your CMP determines who signs off on emergency spending and how you communicate with lenders.

Your BCP protects payroll, close cycles, and reporting obligations when the worst happens.

How crisis management and business continuity plans work together

Treating your CMP and BCP as separate documents is a mistake. They're two halves of the same operational resilience strategy.

Here's how they connect:

- Handoff: The crisis management plan activates first to stabilize the situation. Once immediate decisions are made, business continuity takes over to keep critical operations moving.

- Shared leadership: Your crisis response team and business continuity owners need to know each other. The same people often wear both hats.

- Common communication protocols: Stakeholder messaging, media statements, and internal updates should flow through one agreed channel, not two competing ones.

- Disaster recovery sits inside the BCP: If your systems go down, your disaster recovery plan handles the technical rebuild while business continuity keeps the business functioning through workarounds.

Test them together. Run tabletop exercises and simulations that stress both plans at once. You'll find the seams, the handoff gaps, and the assumptions that don't hold up when business continuity and crisis management collide in real time.

That's the whole point of practicing before the real thing arrives.

Top tips to create a crisis management plan you can trust

This plan is about the first crucial hours and days of a disruption. It's your playbook when decisions need to happen fast.

A useful framework to anchor your thinking is the 5 Ps of crisis management: prevent, prepare, practice, perform, post-crisis.

Here's how to build a crisis management plan that holds up under pressure:

- Identify potential crises. Map every plausible disruption, from cyberattacks and natural disasters to supply chain failure and leadership loss. Rank them by likelihood and impact.

- Establish a crisis response team. Who's in charge? Who handles internal communication? Who talks to the media? Define roles clearly and name backups for each.

- Develop communication protocols. Agree on how you'll communicate internally and externally. Pre-write holding statements for the scenarios you've identified.

- Create actionable checklists. Step-by-step instructions for each type of crisis keep people moving when the pressure's on. Keep them short and readable.

- Run tabletop exercises. Simulations and drills are where plans get stress-tested. Run them at least annually, and invite executives to participate, not just observe.

For finance teams specifically, access to cash is paramount. Build a crisis budget, identify readily available funds, and model scenarios that hit cash flow. Set trigger points that tell you when to act.

Tips to create a business continuity plan

This plan is about keeping the lights on and ensuring your business can continue operating, even if in a limited capacity.

- Business impact analysis. Don't just ask "what's essential?" Map out the entire flow of key processes. Identify dependencies between departments, systems, and data.

- Recovery strategies. How will you recover critical systems and data? Do you have backups? Can you work remotely? Develop detailed procedures for restoring systems and data and make sure you have alternative communication methods if your primary systems are down.

- Alternative workspaces. Do you have a backup location if your office is unusable? Identify specific locations, whether they're remote work setups, co-working spaces, or pre-arranged backup offices.

- Supplier and vendor contingencies. What happens if your key suppliers are disrupted? Have backup suppliers ready.

- Regular testing and updates. Business continuity plans are living documents. Review and update them regularly.

Develop financial models that project the impact of different scenarios on revenue, expenses, and profitability. This will help you prioritize recovery efforts.

Building resilient finance functions takes more than a single plan; it takes continuous learning, the right frameworks, and a network of peers who've been there.

Accelerate your career with Finance Alliance Pro+ Membership and unlock FP&A certifications, pre-built financial models, templates, soft skills workshops, a mentor program, and exclusive access to a community of finance leaders shaping the future of the function.

Frequently asked questions

What are the 5 Ps of crisis management?

The 5 Ps of crisis management are prevent, prepare, practice, perform, and post-crisis.

This framework helps you identify risks early, define roles and action plans, rehearse through simulations, execute during the real event, and then review and refine afterward to strengthen your response for next time.

What are the 4 pillars of crisis management?

The four pillars of crisis management are preparedness, response, recovery, and mitigation.

Preparedness covers planning and training, response is the immediate action during a crisis, recovery restores normal operations, and mitigation reduces the risk of the same crisis happening again.

What are the 4 pillars of business continuity?

The four pillars of business continuity are assessment, preparedness, response, and recovery.

Assessment means identifying hazards and evaluating risks to your critical functions, then layering prevention and recovery measures on top to keep your business running when disruption hits.

What are the 5 Cs of crisis management?

The 5 Cs of crisis management are commitment, clarity, communication, collaboration, and care.

They're the leadership behaviors that separate organizations that come out stronger from those that don't, focusing on how you lead people through uncertainty rather than just following procedures.

Become an FA Insider

Thank you for subscribing

Get exclusive insights, frameworks, and strategies from finance leaders driving real business impact.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn