Finance teams are more than just number crunchers. To become a finance business partner, you must create value by providing insights that help business leaders make data-driven decisions.

But, what is a finance business partner? And how can you (as the CFO) transition your finance team from number crunchers to effective business partners?

Find out in this article, where I share a step-by-step strategy to help you transition your finance team into finance business partners.

Topics covered in this article:

- What are finance business partners?

- Key traits of a finance business partner

- Starting the journey to becoming business partners

- How to create a strategy to transition your finance team to business partners

- The good, the bad, and the ugly of centralizing your finance team

- How to define the core values delivered by your teams

- How to strike a balance between being supportive & being persistent with your board

- Infographic - 5 steps to create an effective business partnering strategy

What is a finance business partner?

As finance professionals, we hate wasting money. Financial planning is one of our key roles. So, naturally, we don’t want to spend money for the sake of it. We want to make sure that every penny is spent in the right place to ensure continuous profitability.

Yet, it’s not always easy (even with all of the financial information and data at our fingertips!). Especially if senior management views you as nothing more than a number-crunching employee.

So, what can you do to transition to a finance business partner?

Well, you must convince the C-Suite that you've got a lot of value to add. And, that your insights are invaluable to the financial health of the business. Thankfully, you won’t have to start fresh out of the gate because finance business partners are nothing new.

Business partnering originated in the HR function. But it has since expanded to include the finance function.

If you want to become a finance business partner, the main goal is to move away from the back office to become a key part of the business. Finance teams need to work with other members of the business as one team to bring the company forward.

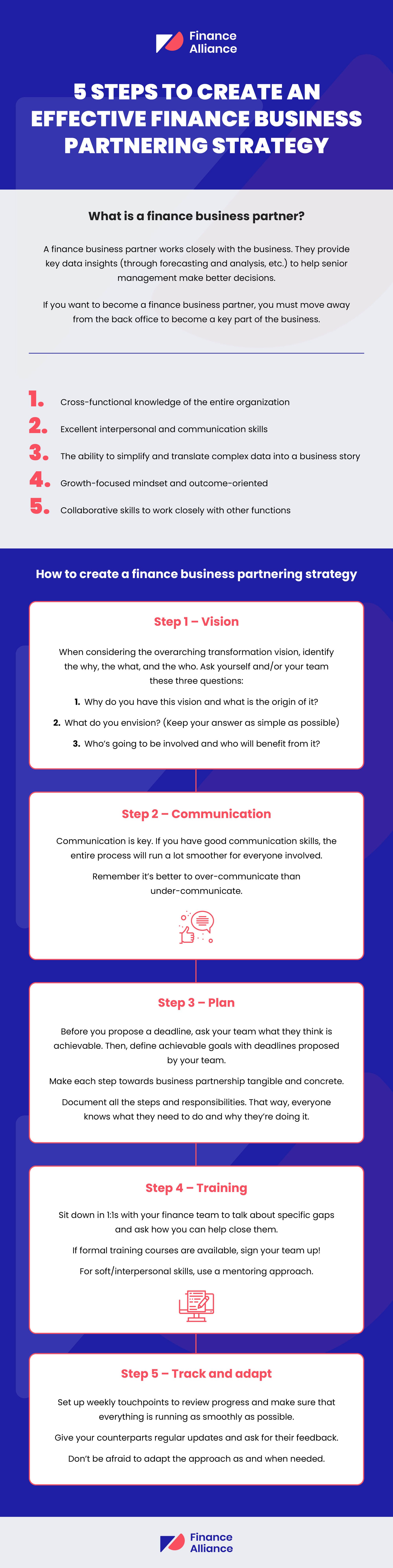

A finance business partner works closely with the business. They provide key data insights (through forecasting and analysis, etc.) to help senior management make better decisions.

Key traits of a finance business partner

To transition to business partners, you must link your finance team with operations. There shouldn’t be a distinct ‘them’ vs ‘us.’ Rather, both functions need to work together. They must use their initiatives and become a joint unit working towards the same goal.

Successful business partners add value to the business. It’s one thing to provide data in a 70-page report. But unless you can simplify the complexity of that data so that others can understand it (and align it with the business model), you’ll find yourself in a constant uphill battle.

You can simplify the data by doing something as simple as using different colors in your financial reporting spreadsheets in Excel. For example, putting the positive data in green, and the negative data in red. Or adding easy-to-read graphs to show how different things are benchmarking against each other.

A growth focus mindset is a belief that you can overcome anything. Rather than seeing something new and walking away from it, you push forward. You learn the key skills to solve the problem.

Another key trait of a successful finance business partner is being outcome-oriented. This is when you’re able to remove the personal component from the situation. You resist the urge to point fingers and you don’t say things like ‘you’ve done something wrong,' or ‘you have a problem.’

Instead, you say things like ‘we have a problem’ and ‘this is how we’re going to solve the problem.’

Focus on the outcome.

To summarise, when someone asks me ‘what do I need to do to become a successful business partner in finance?’ – I list the following:

- Create a link between finance and operations

- Excellent interpersonal skill set

- Provide insights via reporting tools and benchmarking KPIs (not just data)

- Simplifying complexity

- Develop a growth-focused mindset and become outcome-oriented

- Part of the decision-making process

If you can tick all these boxes, you’ll be on your way to becoming a finance business partner who's a key part of the decision-making process.

Starting the journey to finance business partnering

One of the first steps towards transitioning from a ‘number cruncher’ to a business partner is stepping outside of your comfort zone.

As the CFO, you must utilize your leadership skills to help ease your team into the business partner role as smoothly as possible. However, your colleagues may have higher expectations of your finance team than you do.

Therefore, you must prove that you and your team can meet and even exceed their expectations. You must make the conscious decision to leave the comfort zone, not just for yourself, but for your team.

However, getting your team on board may prove more difficult than you thought. As humans, we tend to shy away from change. We like routine and in most cases, we prefer it.

So, what happens when you approach an accountant on your team and tell them that what they’ve been doing for the last 30 years is no longer good enough?

Sure, you won’t say it quite like that. But that’s how they’ll hear it no matter how good you are with your words. It'll make them question their own competencies, whether you’re talking to a Finance Director, FP&A Analyst, or Accountant.

Approaching your team and telling them it’s time for change will provoke some emotions and you may need to make a few reconciliations along the way. It won’t be an easy change, but it’s a necessary one.

It won’t be just you and your team that need to leave their comfort zone for this change to happen. Your operational colleagues will also need to leave their comfort zone. It may not be as dramatic of a change as it will be for you and your team, but it’s still a change nonetheless because you’ll offer them something new.

As your team transitions from number crunchers to business partners in real-time, operational colleagues can no longer hide behind the numbers. You make them responsible for their figures. There are no more excuses. They’ll have to put the effort in and even change the operations as a result.

Transitioning from your current position to a business partner doesn’t happen overnight. It takes time to learn the necessary skills to transition into a finance business partner. They must have a strategist mindset and learn to be adaptive as they transition to what’s essentially a new role.

And, you’ll have to make sure all stakeholders are on board with this transition from the get-go. If relevant stakeholders don’t show much interest in your goal, you’re more likely to run into obstacles preventing further progress down the line.

How to create a finance business partnering strategy

Everyone’s starting point on the journey to business partnering looks different. If I were to use my own journey as a case study, I would emphasize the importance of having a structure and acumen to make strategic decisions.

I created a structured roadmap (of sorts) with several key pillars that proved to be extremely useful:

- Transformation vision (a value-adding finance team)

- Communicate – input from the team and operational colleagues

- Plan – concrete short/midterm actions

- Train – identify and close skill gaps

- Adapt – track implementation and use a feedback loop

Let’s explore each pillar in more detail…

Vision

When considering the overarching transformation vision, identify the why, the what, and the who. Ask yourself and/or your team these three questions:

- Why do you have this vision and what is the origin of it?

- What do you envision? (Keep your answer as simple as possible)

- Who’s going to be involved and who'll benefit from it?

Your answers to these questions will help clarify your overarching vision. For me, that vision was to create a team of finance leaders that added more value to the overall business performance. Having a broad vision like this was beneficial because it kept me focused on the bigger picture. Plus, a broad vision is much easier to remember as it stops you from getting bogged down with finer details.

My advice is to show your team what’s in it for them and convince them that it's worth their time and effort.

For example, accountants can often feel left out of business decisions. If you show them that they can be in charge and make a real difference (and in less time than before), they’ll be more willing to transition from a number cruncher to a strategic finance business partner.

Communication

Communication is key. If you don’t get it right, people will feel left out and won’t be willing to work with you. If you have good communication skills, the entire process will run a lot smoother for everyone involved.

Speaking of everyone involved, you must ensure that all relevant stakeholders are involved from the get-go.

Make your vision their vision.

You’ve also got to keep everyone in the loop. If you can’t convince people to step out of their comfort zone, you'll have a difficult time accumulating the level of support you'll need to succeed.

You need a lot of buy-in and input to get your strategy going. This is true at the start of the journey as well as constant feedback during and after implementation.

Remember that it’s better to over-communicate than under-communicate when it comes to explaining your vision to other people. Go out of your way to ensure everyone feels included and that their thoughts and opinions matter.

Plan

My first tip for creating the plan is to focus on concrete short and mid-term actions. A good place to start is to base the plan on the feedback you received in your first communication loop. This will help you lock down some quick wins at the beginning of the project.

Quick wins in the early stages are important because they motivate you and your team to keep going and follow through with the transition plan.

Before you propose a deadline, ask your team what they think is achievable. Then, define achievable goals with deadlines proposed by your team.

When you talk about the vision, it can be very vague and difficult to grasp. You need something tangible and concrete when you create your plan so that everyone knows what steps and tasks they need to complete. I recommend documenting all the steps and responsibilities. That way, everyone on your finance team knows what they need to do and why they’re doing it.

Once you have this timeline, share it with your stakeholders and operational colleagues. Don't prepare something, dump it on the table and run away. Start a conversation and distribute the timeline to all stakeholders. Give them an idea of what the timeline looks like.

Training

For training, begin by identifying skill gaps and then take the necessary actions/steps to close those gaps. To do this, seek feedback from your team about which topics they’re most uncertain about. Then, overlay this with the feedback you’re getting from your counterparts and your perspective.

Sit down in 1:1s to talk about the gap and ask how you can help them close it. If formal training courses are available, sign your team up for them and talk about it in the next team meetings. Focus on improving performance management and if there are areas to introduce automation to help make things easier for your team, discuss them.

For soft/interpersonal skills, use a mentoring approach, preferably with someone outside the F&C function.

Mentoring is also a sign of appreciation. Every employee I've ever mentored or mentored was very grateful for it. Plus, it doesn't cost you a penny and it makes a massive difference to your team, motivating them to grow both personally and professionally.

Track and adapt

Ultimately, you need to stay open-minded and flexible. Yes, you can create a strategy that seems flawless on the outside. However, it also needs to be flexible enough to survive the unexpected. You need a flexible strategy that can adapt to change with ease.

Set up weekly touchpoints to review progress and make sure that everything is running as smoothly as possible. Give your counterparts regular updates and, as I mentioned previously, ask them for their feedback.

If something isn’t working, have an open discussion about why it’s not working. Is there something you can do to improve the existing strategy?

Centralizing your finance team: The good, the bad, and the ugly

Centralization is one of the best ways to structure decision-making within a finance team. But like most things in life, centralizing your team comes with both advantages and disadvantages.

Here are some of the main benefits of centralizing your finance team:

- Implementation of accounting standards across the group

- Great communication and sense of belonging within the F&C team

- Efficiency and cost savings

- Focus on the joint vision

- Quick turnaround of decisions

On the other hand, centralizing your finance team comes with a few disadvantages…

- Less sense of ownership

- More specialization leading to less general knowledge

- Disconnect from the operational colleagues

- Potential for more friction between the finance teams

Financially, centralizing your finance team is worthwhile and there are a lot of upsides to doing so. However, I’d be lying if I said it was going to be smooth sailing and there are some downsides to centralization.

Deciding whether to centralize your finance team is a decision you should make with confidence, which is why it’s good to be aware of both the positive and negative sides of centralization.

How to define the core values delivered by your teams

You’ve probably heard your fair share of corporate values. However, if we’re honest with ourselves, corporate values are fairly meaningless.

So, how can you give corporate values meaning?

My advice is to link your vision to your corporate values. It also helps to find examples of what the values mean in a specific finance context. Here are a few examples:

Integrity: In finance, we don’t book anything that is against good accounting practices to enhance the results.

Customer focus: In finance, we work on problems together with our operational colleagues (define your internal customers)

Ask your team what the values mean to them so you can share a few examples. By sharing examples of how these values impact everyday life, people are more likely to act on those values and remember them.

The next step is to incorporate these mantras into your presentation master template and email signature.

How to strike a balance with your board (support vs persistence)

You can’t transition your finance team into business partners without becoming a business partner yourself.

As the CFO, your team looks to you for guidance. You’re the example they’ll come to follow, which means you need to think about how you can add the most value to the business.

Here are a few of my top tips for CFOs who want to strike a good balance with board members:

- Board rooms are often very competitive and sometimes confrontational

- Understand where your colleague is coming from

- Put your ego aside and prioritize what’s best for the business

- Always stay open to compromise unless it goes against your integrity

- After thoughtful consideration: It’s okay to say no

Infographic - 5 steps to create an effective finance business partnering strategy

Here's a handy infographic detailing the 5 steps to create an effective finance business partnering strategy - enjoy!

I hope these insights and tips help you to transition your finance team from number crunchers to business partners successfully.

Become an FA Insider

Thank you for subscribing

Get exclusive insights, frameworks, and strategies from finance leaders driving real business impact.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn