Jon Cochrane, VP of Strategy at Maximo, gave this presentation at the CFO Virtual Summit, 2023.

Understanding how to optimize cash is very important, especially in today’s current market. If you know how to optimize cash flow in a business, you’ll be in a much healthier position financially with more accurate forecasts.

In this article, I share some of the best practices for optimizing cash flow forecasting.

So, if you want to know how you can transform your finance operation into a strategic asset, keep reading!

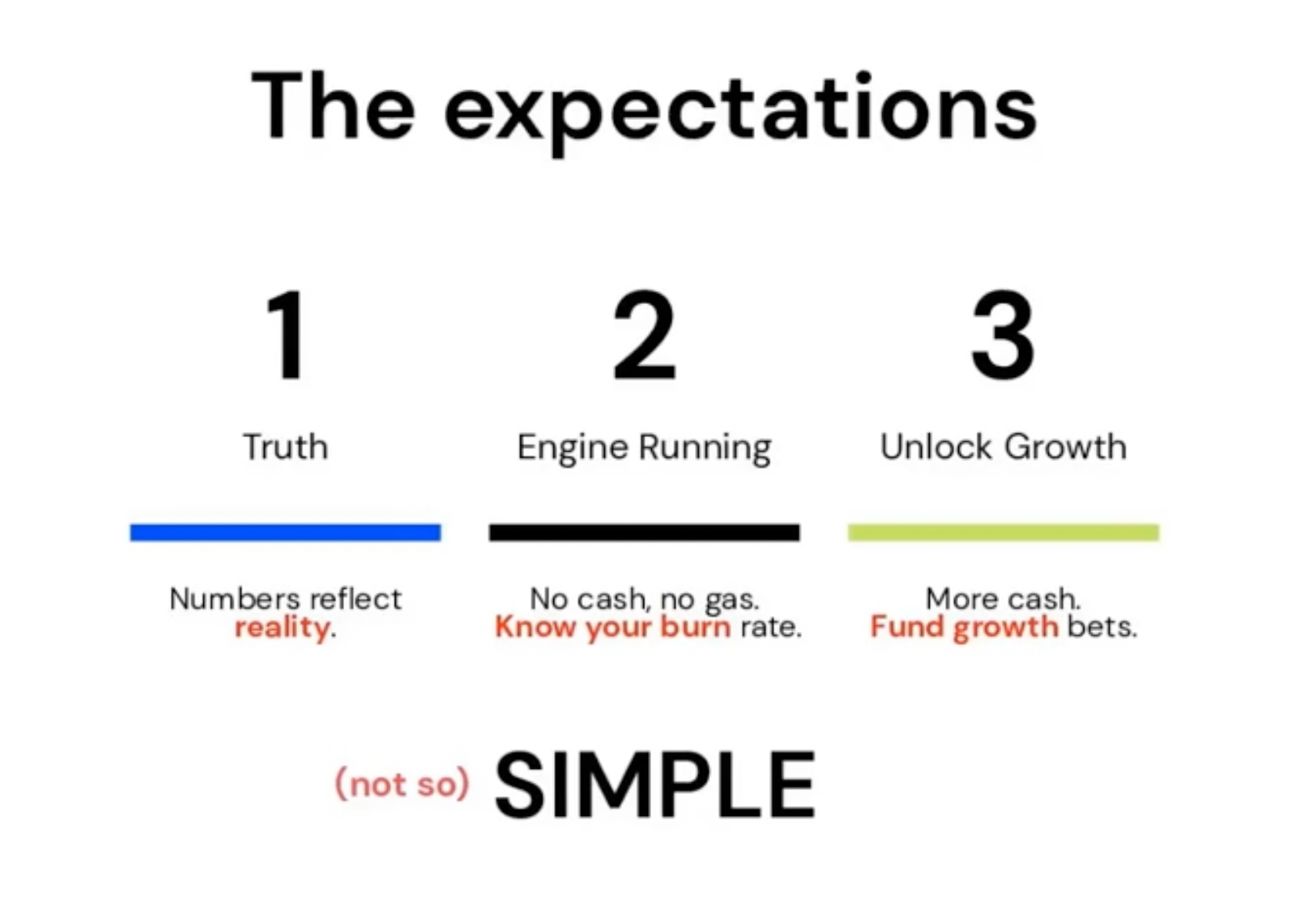

What’s expected of finance leaders

One of the things that we've seen at Maximo, and more broadly in the industry is that finance leaders have BIG expectations placed on them.

Here are just a few:

The truth

First and foremost, finance leaders are expected to be the source of truth. They own the real business numbers.

If we’re honest, we must admit that sometimes, the numbers that come from other departments aren’t always correct. Most importantly, they don’t always inform the best decisions, especially when it comes to the financial health of the business.

Keep the engine running

Finance leaders are expected to keep the engine running. We’ve always got to make sure that cash coming into our business is always going to be greater than the cash that's in the bank today.

Unlock growth

In the past, it was more traditional for finance leaders to come through an accounting path or something similar. Nowadays, though, we’re seeing a shift in finance as more CFOs and other finance leaders are tasked with finding ways to unlock growth in their businesses.

Operation-orientated CFOs are more common, particularly when they’ve come from FP&A because they’re looking to the finance department to help the company unlock future growth.

The expectations of finance leaders

Living up to and even exceeding these expectations isn’t easy. When it comes to financial forecasts, if bad data goes in, bad cash forecasts come out.

If you don't have a solid handle on the data coming into your business, you won’t be able to make solid decisions about the future state of the cash flow in your business.

So, it's important to have a good pulse on the data, including your invoicing workflows, your DSOs, and all the different things that impact your cash forecast.

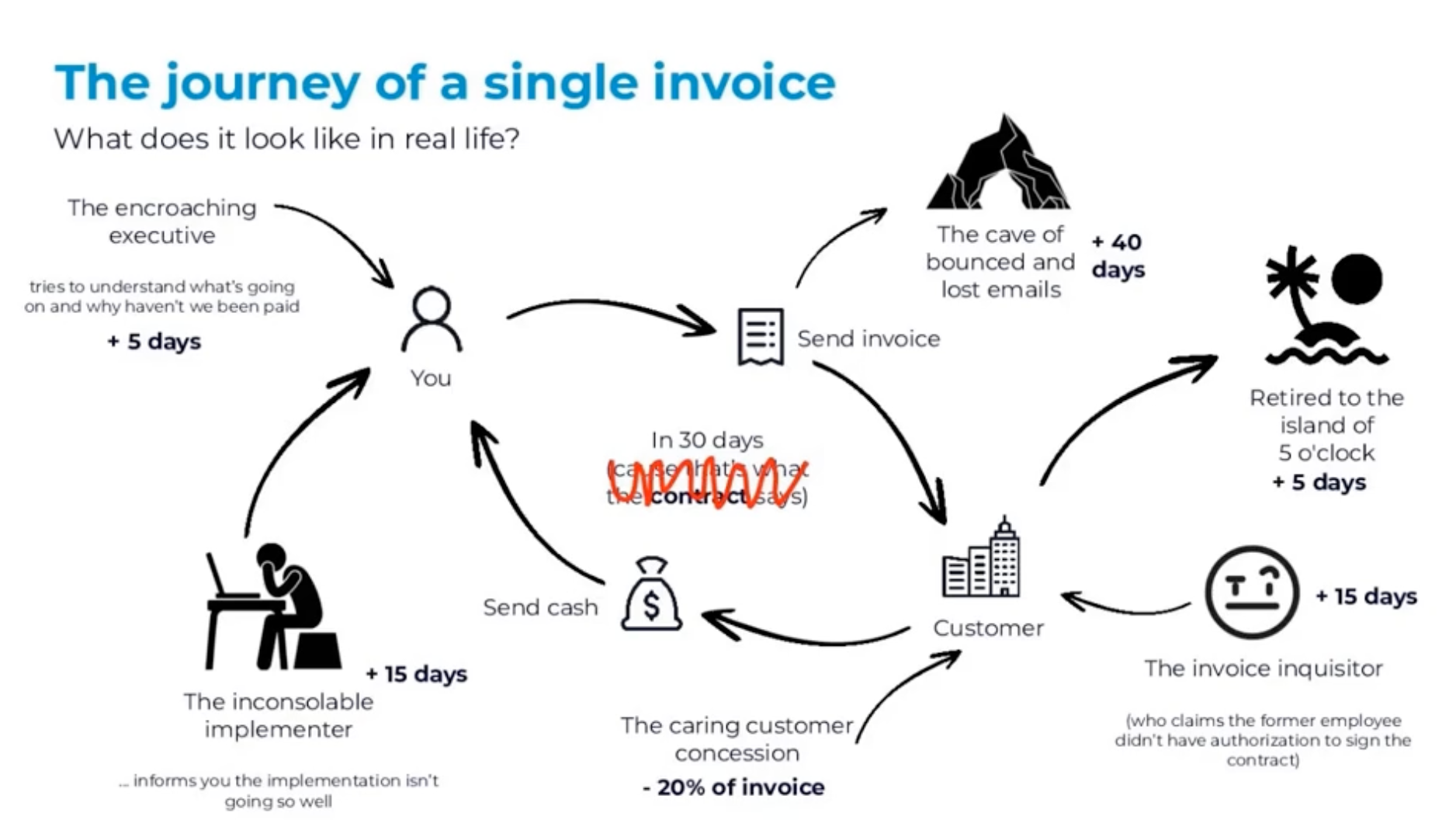

The journey of a single invoice

Managing a single invoice in your company can be a challenge, especially when you have hundreds or even thousands of invoices to manage.

Below is a visual representation of the journey of a single invoice:

The invoice journey begins when you send an invoice to the customer. Ideally, they’ll send you cash within 30 days, because that's what a contract says. However, it’s not uncommon for the invoice to not make it to the customer.

If that happens, many times, businesses don't find out about it until 40 days after the invoice has been sent. This is usually because the invoice was due in 30 days, and it only pops on your radar once the due date has come and gone.

Of course, this then leads to further issues. By the time you realize the invoice hasn’t been paid or it hasn’t reached the customer, your primary billing point of contact may have moved on. They may have retired, moved to another business, or someone else may be in charge.

The next thing you know, you’re dealing with another executive or team member who's looking at the invoice and questioning why they’re paying this amount to this company. You will then need to answer their questions.

So, how can you manage an engine like this to ensure you can manage invoices and put an accurate cash forecast together?

Well, it comes down to three things…

1. Automate billing and collections

When a customer closes a new contract, how quickly do you get the invoice to the customer?

If you can get it done on day zero, which is what the best companies do, then many times, that cycle of the unpaid invoice never becomes an issue. This is because they are invested in your technology and platform. After all, they’ve paid for it. Automated billing helps reduce unpaid invoices.

You also need to consider your collections strategy. If you want to have a fine-tuned cash engine, you need a strategy.

Making sure that you've got a predefined game plan for managing your collections and identifying and mitigating high-risk invoices is so important. By high risk, I’m talking about invoices that haven’t been paid for 60 days. Put those under a magnifying glass and make sure you’ve built a solid process around automating billing and collections.

2. Close A/P before next month

You must be able to close A/P before the next month begins, which can be a bigger challenge than you might think. You should have a pulse on all of your recurring expenses such as your payroll, rent, data center costs, bonuses, commissions, etc. If you can do that, you can close A/P before the end of the month. Closing A/P by the end of the month tells me you've got a really good pulse on what’s your cash out.

3. Measure you’re A/R health

When it comes to cash, you've got to measure your A/R health, which comes down to two things.

The first is DSL (day sales outstanding), so counting how many days it takes a customer to pay you after you’ve sent an invoice. There are different ways to measure DSL, but it’s essentially an estimate for figuring out how many days it takes somebody to pay you. You should be tracking that monthly. If that number ticks up, it's an indicator that you've got a problem in your cash flow engine.

The second thing to measure is your A/R health. To measure this, you can track or count the percentage of invoices that were saved below a certain number of days outstanding, versus the percentage of invoices that have been outstanding, say more than those days.

If you're doing these three things as regular occurrences, you're hitting the best practices to ultimately forecast your cash flow. So, as long as you’re doing these three things, you can make sure you’ve got good data in, which ensures you have good data and predictions going out.

How to do a cash flow forecast

If you've never done a cash flow forecast before, a good place to start is with a 13-week cash flow forecast. This is a great way to give you a pulse point on what your cash is today. It also shows you what your cash flow looks like over the next three months.

When you have a good pulse on your next three months, you can then create your annual forecast or a rolling forecast that you can use to forecast your cash out over the next 12 months.

Here’s how it works:

Starting point: Understanding your current bank balance

Firstly, get a clear picture of your current financial standing. Log into your bank accounts to assess your current balance.

Knowing your bank balance is like having a pulse on your financial health – essential for any business.

The next three months: Forecasting cash inflows and outflows

Forecasting is key. Look ahead to the next three months and list out potential cash inflows and outflows. This includes payments from invoices (a primary source of income for most businesses), payroll, rent, marketing costs, and payments to vendors. Remember, your assumptions in this stage are crucial.

3 tips for cash flow forecasting

- Automate billing and collections: Streamlining these processes ensures quicker cash inflow.

- Close Accounts Payable (AP) promptly: Regular closing of AP helps avoid surprises in cash outflows.

- Monitor Accounts Receivable (AR) health: Keep track of the money owed to your business to maintain a healthy cash flow.

Finance alliance insider

Thank you for subscribing

Level up your finance alliance career & network with finance alliance experts.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn